Average Cost of Electricity for PG&E Now Higher Than During California Energy Crisis

Average Cost of Electricity for PG&E Now Higher Than During California Energy Crisis

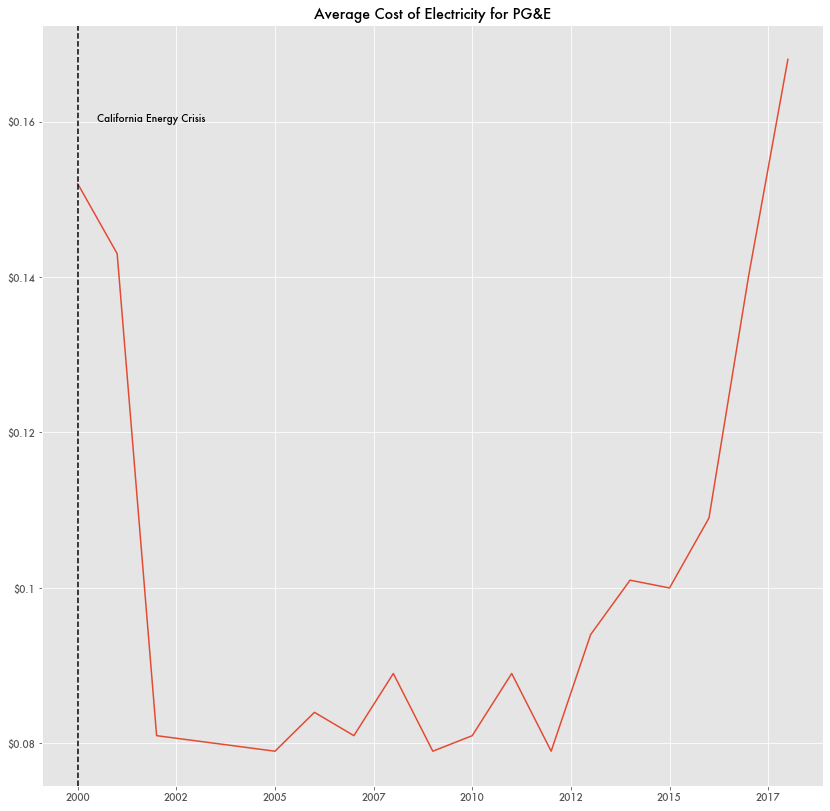

The average cost of purchased electricity for Pacific Gas & Electric (PG&E) is now more than what it was during the California electricity crisis of 2000-2001.

According to annual reports, the average cost of purchased electricity for the utility was ¢16.8 per million kilowatt-hours (kWh) in 2018. In 2000, it was ¢15.2. In the 18 years between then, the price hovered close to 10 cents.

The company ascribed the increases since 2012 to demand but also “the higher cost of procuring renewable energy” to comply with California law. In 2002, California established the Renewable Portfolio Standard Program that would increase the percentage of renewable energy as a source of electricity, and that percentage goal has only been increased since.

California has also seen the decline in nearby generation resources since 2012: the shutdown of the San Onofre nuclear facility, the Navajo generating station, and the Aliso Canyon natural gas storage field—site of a major gas leak in 2015.

While electricity for the utility is expensive, natural gas—a major source of electricity generation for the state of California—is currently cheap. Prices at the Henry Hub have varied between $2.5 to slightly over $3 per million Btu in recent years, more than a dollar cheaper than what it was in 2000.

Similarities to the Crisis

In 2000, electricity prices like these were considered extraordinarily high, leading to the bankruptcy of state energy utilities and energy markets, rolling blackouts throughout California, and a lengthy investigation of price manipulation by energy traders.

And similar to 2000, California recently implemented widespread rolling power outages, and the Department of Energy announced a state of emergency for California as a summer heat wave led to a shortage of natural gas.

As a result of the bankruptcy in 2001, PG&E sold off $11.9 billion in bonds in what was at the time the largest bond sale in U.S. history to cover long-term energy contracts signed in 2001, and some of the bond payment costs would be passed on to ratepayers.

The utility also entered bankruptcy again, although unrelated to high electricity costs, to shield itself from penalties stemming from major wildfires and has been in ongoing negotiations with the hedge funds that are its major bondholders. Over the last ten years, hedge funds have taken a much larger investment in PG&E, raising their ownership in the stock 24-fold since 2010.

But while the 2000-2001 crisis led to outrage, investigations and lawsuits, recent price spikes haven’t had the same effect, largely because California residents are paying more.

In the midst of the 2000-2001 crisis, the California Public Utility Commissions (CPUC) raised electricity retail rates, which were previously fixed, and ratepayers throughout the state were hit with a large increase in power bills for years to come.

Despite the high revenues from higher retail rates, the utility struggles with being severely undercapitalized amid the bankruptcy, wildfire claims, bond payments, and high electricity rates.

The 2000-2001 California Energy Crisis Redux

Beginning in the summer of 2000 and extending into 2001, California utility companies like Pacific Gas & Electric (PG&E) and San Diego Gas & Electric (SDGE) were hit with increased demand for electricity and a decreased supply of energy due to a large drought affecting hydroelectric power generators as well as the state’s limited generation capacity and limited credit at the time.

The state had recently deregulated its electricity markets a few years prior, creating trading markets for energy companies to bid competitively. Previously, markets were relatively fixed and controlled by the utility companies. The push to deregulate the markets and open them up to competition was done ostensibly to drive down electricity prices by taking advantage of competitive pricing for natural gas, which was relatively high compared to other states at the time.

But during the summer of 2000, prices began skyrocketing past what might be expected. Reports following the crisis would point to a host of causes such as a lack of hydroelectric power in the Pacific Northwest caused by drought. California’s market was deregulated haphazardly, and utilities rarely used futures contracts to buy energy or electricity and regularly relied on the more volatile spot markets for pricing.

But eventually the focus would turn to price manipulation by energy traders.

Enron Takes the Blame

Most of the blame for the energy crisis would eventually be pointed at Enron, the Houston Energy trading company that would go bankrupt a year later. Enron was accused of manipulating California energy prices that drove the crisis. Recorded conversations of Enron traders showed a callous attitude to the individual consumers suffering from the blackouts and coordinating the shutdown of generating facilities to drive up demand.

Memos would reveal trading techniques such as “Incing,” “Ricochet,” “Fat Boy,” and “Death Star,”—no relation to the Star Wars terms that would appear in Enron’s accounting scandal—to avoid state price caps or get paid for transferring energy that legislators pointed to as evidence of price manipulation.

Enron denied the manipulation charges and pointed to the high prices as a result of the energy shortage. In a letter sent to then Vice President Dick Cheney, Enron CEO Ken Lay wrote that he believed prices would go down with increased competition and that the high prices would encourage more entrants into the market and more natural gas supply, but price caps should be avoided at all costs.

But FERC would institute price caps in 2001. Soon after, electricity prices in California would level off and Enron would enter bankruptcy soon afterwards.

A few years prior to the crisis, Enron had acquired Portland General Electric, which provides hydroelectric power that was sometimes sold to California. The merger was unique in that it received the blessing of environmental groups like NRDC at the time. Environmental groups, like NRDC and Environmental Action Foundation, also supported California’s energy deregulation in the 90s under the assumption that it would help encourage reducing energy-related pollution.

While FERC eventually settled with Enron for $1.5 billion and the company admitted to publishing false information, the agency never gave explicit proof that the company’s actions were the main cause of the price spikes, and Enron claimed their trading strategies were common practices and not that nefarious. Other energy companies pointed to the state’s credit issues as a cause for high prices.

In a FERC report on the crisis, the agency noted one firm, Reliant, as singularly responsible for “high-volume, rapid-fire trading”, referred to as “churning” which “significantly increased the price of gas in that market.” Reliant was also indicted for manipulating prices by intentionally closing plants during the crisis—something Enron was accused of co-ordinating but not prosecuted for—and eventually settled for $460 million.

While Reliant’s trades were with Enron via Enron Online, the company’s online market trading portal, Reliant was considered the instigator of the trades. Enron was simply the broker in a many-to-one market platform. Enron Online was castigated by FERC for giving Enron inside information that it could profit off of and enabling Reliant’s wash trading.

Almost every other energy trading company operating in California except one, Williams Energy Marketing & Trading Co., were accused by FERC for their actions at the time, mainly for publishing false prices.

Another company trading in California’s energy market and Enron’s closest competitor, Dynegy, was implicated in the crisis, and would eventually settle for $281 million, but the company would also collapse in ways not so different from Enron, with an accounting scandal, the shutdown of its online energy trading platform, and eventual bankruptcy.

A natural gas seller, El Paso Energy, was accused of constraining capacity to drive up prices, and they would eventually be fined $2.1 billion, more than that of Enron. The company would eventually be bought up by Kinder-Morgan, a gas pipeline company headed by an ex-Enron executive, Richard Kinder, that bought up Enron’s pipeline business out of bankruptcy.

The market manipulation accusations wouldn’t stop there. More than ten years after the fact, numerous other energy traders that weren’t originally named in the original FERC investigation, like Koch Energy Trading and Shell Oil, would be accused of Enron-like manipulation for their roles in the 2000-2001 crisis.

Enron’s Political Influence

Besides the manipulation accusations, Enron was accused of creating the crisis by lobbying for deregulation policies that enabled it all to happen.

The chairman of FERC at the time, Pat Wood III, was accused of having close ties to Enron’s chief, Ken Lay, and both were avid supporters of the deregulation that set up California’s trading markets. Enron was a large supporter of Phil Gramm, the Texas Senator, who led the passage of the bill to deregulate energy commodity markets that enabled the creation of Enron Online, and his wife, Wendy Gramm, was on Enron’s board after serving as a chairwoman for the Commodity Futures Trading Commission (CFTC).

That bill, the Commodity Futures Modernization Act of 2000, included what was referred to as the “Enron Loophole,” which exempted certain types of energy derivatives contracts from regulation. In particular, it exempted bilateral contracts not on an established trading facility as long as the transactions were between “eligible market participants”—certain legal entities satisfying capital thresholds and other requirements. The loophole essentially allowed the kind of over-the-counter trading (OTC) of energy futures done on Enron Online. The loophole was effectively closed in 2008 through legislation included in that year’s Farm Bill.

In the end the close ties with the FERC commissioner didn’t help and the agency didn’t hold back in its punishment of the energy giant. But because of the company’s eventual bankruptcy the company was only expected to pay approximately $260 million.